Please consider signing this petition, to make HDFC Bank listen and do the right thing

If you came here from the Day 60 update on Twitter, I’m sorry… that was an April 1 prank where the joke is on us customers and played by HDFC Bank. That should be ‘continued to be played by’, on second thoughts.

Before you read – please see the sequence of points in this post:

14. [May 15, 2017] I had written to the Government’s Consumer Helpline about this unethical practice by HDFC. HDFC Bank has responded and closed my complaint. With this!

13. [May 9, 2017] FINALLY! A figleaf to hold on to! An auto-response (weak, I know, but hey, there’s at least an acknowledgment to hold on to!) from RBI where they have forwarded (!!) my complaint to HDFC’s Banking Ombudsman nodal officer!

12. HDFC Bank did *something* about this unethical mess, but it is as lame and evasive as its response so far!

11. Relevant citings and excerpts from RBI, Banking Codes & Standards Board of India (BCSBI) and media.

10. HDFC’s Corporate Communications Head, Neeraj Jha responds, on Facebook. + My response to his points.

9. What can you do, if you are impacted too, as a HDFC Bank customer, or simply as an annoyed bank customer in India

8. A list of other HDFC Bank account holders who are as surprised as I am, about this unethical charge

7. My email to all the Board of Directors of HDFC Bank

6. My email to HDFC’s own Banking Ombudsman Nodal Office, Binod P

5. My email to RBI’s Banking Ombudsman #1 and #2

4. Other publications/blogs on this issue

3. My perspective on HDFC Bank’s response (that I have emailed in response)

2. HDFC Bank’s response to my query about this unethical practice

1. Original blog post that explains what HDFC Bank is indulging in

1. Original post

My first salary was credited to a HDFC bank account. In New Delhi. I have since had HDFC accounts—salary, personal, home loan, car loan, you name it—for over 2 decades.

Now, I’m not adding these details to sentimentalize this post. (Oh well, that first salary part is a bit maudlin, I accept!). The point is, there’s way too much banking between me and HDFC that I can’t wash them off if the need arises and move to another bank, without a lot of wasted time and effort. So, why am I even considering that?

Let me explain what the problem is, first.

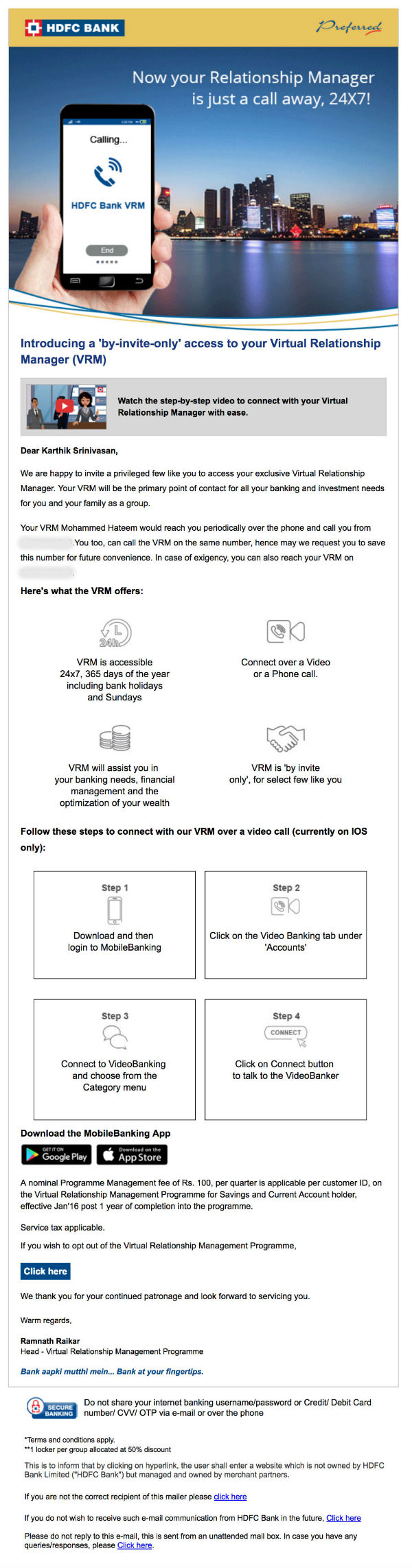

I received a mail from HDFC Bank on January 30th. The subject said,

“Dear Karthik Srinivasan, Welcome to HDFC Bank Preferred Banking Programme!”

I get at least 2-3 emails from HDFC every week. All of them ensure that they call me a ‘preferred’ banking customer. This has been going on for over 2-3 years, if I recall right. Now, I have no idea what this ‘preferred’ banking entails. I’m totally open to the possibility that I was shown a laundry list of fine print when this account was opened and I may have signed it too.

Anyway, I opened the mail curiously, to know why I’m being welcomed into something that I’m adequately a part of. This was the entirety of that mail.

Crux: an invite-only program where a virtual relationship manager has been assigned to me.

My first thought: Oh great! The once-every-2-years that I actually call someone from HDFC bank can be slightly easier now!

Then, I notice this.

A nominal Programme Management fee of Rs. 100, per quarter is applicable per customer ID, on the Virtual Relationship Management Programme for Savings and Current Account holder, effective Jan’16 post 1 year of completion into the programme.

Service tax applicable.

If you wish to opt out of the Virtual Relationship Management Programme,

Click here

What?

Let me deconstruct that.

I was enrolled into this ‘program’ in January 2016. After a year of being in the program that I did not ask to be enrolled into and have no recollection of being in (I did check my emails from 2015, in December, and 2016, in January and February, as also emails from HDFC when I had opened this account), I will, from now on, be charged Rs.100 per quarter to be in this program.

And, service tax extra.

What cheesed me off is not the nominal amount. It was,

If you wish to opt out of the Virtual Relationship Management Programme,

Click here

This is an opt-out program.

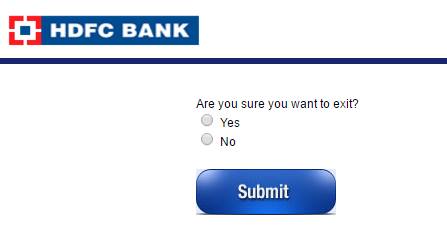

So, I clicked on the link and performed the 2 actions needed to unenroll myself out of this invite-only program that presumes I’m already in.

In simple terms it means, HDFC depends on a customer’s action to not charge him/her. The usual, sane and honest method is, ‘HDFC depends on a customer’s action to charge him/her’. It means HDFC seeks consent to charge a customer. What they are doing is seeking consent to not charge a customer.

In other words, HDFC depends on the customer to,

1. open the mail,

2. read through the contents,

3. notice a way to opt-out,

4. click the opt-out link,

5. choose ‘No’ as confirmation and

6. submit the form

… to not charge him/her.

If the customer doesn’t perform even one of the above 6 tasks, he/she will be charged.

To make it even more explicit, figuratively, HDFC presented me with the following:

“I, Karthik Srinivasan, agree to pay Rs.100 (plus service tax) per quarter towards the Virtual Relationship Management Programme. Unless I click on the button below to indicate my preference not to be part of this program, I’d be charged for this service.”

This is clearly unethical and disingenuous.

It particularly hits home for me because I was in Flipkart, handling their corporate communications when they faced a similar issue. Back in 2012, when Flipkart launched the ‘save credit card’ feature (where customers have an option of saving their credit card details for easy payment in the future) after getting a PCI-DSS certification, they rolled out the feature where the check-box for saving the card is checked, by default. This is a classic opt-out tactic that is known to increase sign-ups/uptake of whatever program you are running.

It means, customers, who are previously unaware that Flipkart had a ‘save-card’ feature now need to take note of this feature and uncheck that box to opt out of this feature. In other words, Flipkart had pre-decided that customers want to be a part of it. And unless a customer explicitly asks not be part of it (by unchecking the box), they will continue to be part of this.

After this service was launched, there was a lot of hue and cry about Flipkart’s unethical practice in rolling out this feature. What was truly admirable, back then, was the fact that Flipkart not only acknowledged this error in judgement and set right the process (to opt-in; that is, give customers an unchecked box and let them exercise the option to be a part of this program, or not), but they also blogged about both the error and the reason why they changed it.

Here is the , from 2012.

HDFC is treading a far more dangerous ground. Flipkart did not charge money from people who forgot to opt out. They merely saved some data without explicit consent. HDFC, in this case, is going to take money from people who may have either ignored the mail, or forgotten to see the message about opting out in the mail. I’m fairly sure there are RBI guidelines that determine that any charge levied on the customer should be done after seeking explicit permission to do so. That is, after explaining to the customer that they are going to be charged for specific services. And not merely inform a customer that they’d be charged from now on for a service and only if they choose not to be part of it, will they be left alone without a charge.

The irony is that this HDFC mail starts by calling it an ‘invite-only’ service. The crucial point is that my option to decline the invite hinges on my opening and reading this email fully, and taking appropriate action.

I emailed HDFC Bank asking them why this is an opt-out and not an opt-in. I tweeted to them too. I got the following response after 2 days.

They have merely reiterated the status quo to me – that this is what it is, but hey, we did give you an option to get out of this scheme and about being charged. Tough luck if you didn’t read the mail.

You could ask me a question based on ‘caveat emptor’ (buyer beware), which says, ‘that the buyer alone is responsible for checking the quality and suitability of goods before a purchase is made’. The argument could be, I, as a customer, should be vigilant and alert enough to go through all communication from my bank and take note of the charges proposed to be levied on me and communicate my intent to agree or disagree appropriately. This is a fair argument, but let me present how it may look like, in the real world.

You enter your favorite, and usual, cloth store. You try out 3-4 clothes and decide that you don’t like the fit and decide to try another store. As you walk out, the sales guy calls you back and says that you need to buy them. You ask him why. He says that the price tags in each of the clothing pieces you tried have a fine print that if you try them, you’d need to buy them too. That your trial amounts to a legal contract between the seller and buyer. This is opt-out. If it was opt-in, before you enter the trial room, a store person would have told you the rules and sought your consent.

If you have got this email, or recall being in something called ‘Virtual Relationship Management Programme’, please do check your email and take action based on your interest and intent.

So, considering all this, and the effort it’d take for me to close *all* my HDFC accounts and move to another bank, I’m not going that route. Instead, I’m going to try another route – to try and make HDFC own responsibility for this lapse in ethics and apologize, not just to me, but in public, to all their customers.

I’m going to share this blog every single day for the rest of the year – one day in the morning and the next, in the evening (and so on) on Twitter. And once every week on Facebook and LinkedIn for the rest of the year. I’ll tag relevant people to each tweet/post as necessary to ensure that it is read and understood by as many people as possible.

I’m very curious to see if my bank has an ethical stand on this issue at all.

2. HDFC Bank’s email response to my query

I received a couple of calls from HDFC on February 3, 2017. They tried to convince me with the content of the tweets (above) and after my telling them repeatedly and firmly (and politely) that I’m not convinced and that they are merely repeating the same thing again without addressing what I’m alleging, they sought 2 days’ time to revert. There was no response after 2 days, so I continued my daily updates on Twitter.

Then, on February 9, 2017, I received the following email.

3. My perspectives on HDFC Bank’s email response

My issue remains the same, while I fully appreciate all the efforts from HDFC in improving the benefit for customers.

1. Regarding testing the service for 1 year – I have no recollection of any communication from HDFC about launching VRM for me. I keep getting a call from ICICI or HDFC that says, ‘Sir, we have appointed a dedicated service manager for you and he’d like to come and meet you’. I say that I’m not interested, every single time.

2. The opt-out experience is the fundamental crux of my blog post above. I have explained in detail how disingenuous it is. If it complies with regulatory requirements (I HIGHLY doubt it would, particularly when customers are charged), it still doesn’t mean it is ethical. HDFC is looking at compliance, I’m talking about ethics. Vastly different topics.

3. I have never, ever received communication on charges for VRM. Most comments in this blog post, and on Twitter, point to many people not having any awareness about this charge.

4. The laundry list of ‘key benefits’ for a ‘nominal’ Rs.100! Wow! Where did this list suddenly materialize from? You see the original opt-out mail from HDFC, above? Doesn’t that portray that the Rs.100 charge is *just* for VRM? But now, miraculously, there are many more benefits for Rs.100. I’m sorry, but the point is still the same – please explain these to your customers, and let them agree to pay the charge per quarter consciously. Do not just take the money off their accounts just because you believe that the ‘nominal’ fee’s benefits far outweigh the charge. Let people, who actually own the money, decide that.

4. Other posts on HDFC’s unethical move:

1. .

2. This blog post carried in

3. Dhirendra Kumar of Value Research writes in (March 6, 2017)

4. How HDFC Bank may discretely charge you for new ‘services’ and how you can avoid it ()

5. Dhirendra Kumar, in Value Research website: 6. A Well thought (but misguided) Strategy or a Scam – Program Management fee for HDFC Classic and Preferred accounts ()

5. My first email to RBI’s Banking Ombudsman ()

Sent on February 11, 2017 – To C.R.Samyuktha, as mentioned in RBI’s Banking Ombudsman website.

Email ID: bobangalore@rbi.org.in | Status: No response or complaint acknowledgment as on March 26, 2017

***

My second email to RBI’s Banking Ombudsman ()

Sent on March 11, 2017 – To C.R.Samyuktha, as mentioned in RBI’s Banking Ombudsman website.

Email ID: bobangalore@rbi.org.in AND CC: Chief General Manager, Consumer Education and Protection Department, RBI (email ID: cgmcepd@rbi.org.in) | Status: No response or complaint acknowledgment as on March 26, 2017

6. My email to HDFC’s own Banking Ombudsman Nodal Office, Binod P, listed in HDFC’s website:

Sent on March 27, 2017 – To Binod P, as mentioned in HDFC’s corporate website.

Email ID: bohdfcblr@hdfcbank.com

7. My email to all the Board of Directors of HDFC Bank (details, including email IDs, here)

Sent on March 11, 2017.

To:

Mrs. Shyamala Gopinath – chairperson.bod@hdfcbank.com

Mr. Partho Datta – Pdatta.bod@hdfcbank.com

Mr. Bobby Parikh – Bparikh.bod@hdfcbank.com

Mr. A. N. Roy – Anroy.bod@hdfcbank.com

Mr. Malay Patel – mpatel.bod@hdfcbank.com

Mr. Keki Mistry – Kmistry.bod@hdfcbank.com

Mrs. Renu Karnad – Rkarnad.bod@hdfcbank.com

Mr. Aditya Puri – Managingdirector@hdfcbank.com

Mr. Paresh Sukthankar – Psukthankar.bod@hdfcbank.com

Mr. Kaizad Bharucha – kbharucha.bod@hdfcbank.com

Mr. Umesh Chandra Sarangi – Usarangi.BOD@hdfcbank.com

Mr. Srikanth Nadhamuni – Snadhamuni.BOD@hdfcbank.com

Status: Acknowledgement received on March 16 | No response (beyond acknowledgement) as on March 26, 2017

8. A list of other HDFC Bank account holders who are as surprised as I am, about this unethical charge

1. Here is Rashmi R Padhy talking about the same opt-out problem with regard to a Classic Banking Program.

2. Here is another customer of HDFC mentioning that the opt-out link did not work for him!

3. Here’s Raveesh, freshly after getting HDFC’s mail.

4. Here are 40 more people (click on the thumbnails for complete list).

5. Here are a lot more utterly annoyed and surprised customers of HDFC Bank who are wondering about the mysterious Rs.100 + taxes that they accidentally found out from their statements: On Consumer Complaints website.

6. A lot of surprised customers debating this unethical charge on DesiDime website.

9. What can you do, if you are impacted too, as a HDFC Bank customer, or simply as an annoyed bank customer in India

Option 1: Write to the RBI Banking Ombudsman – .

The text of what I wrote, in case you need it, is here. You may copy-paste and edit it as you want.

Option 2: Write to all the Board of Directors of HDFC Bank – details here.

The text of what I wrote, in case you need it, is here. You may copy-paste and edit it as you want.

Option 3: Write to foundation@moneylife.in – hope this can help Sucheta Dalal and MoneyLife to pursue this via RBI and get HDFC Bank to not only stop this devious tactic, but also apologize to customers publicly.

Option 4: Sign the Change.org petition created by Sucheta Dalal that addresses this particular point (unethical charges) among many other points: Petition · Governor: RBI-Finance Ministry: Stop Banks Fleecing Depositors http://bit.ly/2nI6EPY

10. HDFC’s Corporate Communications Head, Neeraj Jha wrote on his Facebook page:

Here is my response to his points:

a) Giving the customer the opportunity to experience the service for free for a year before levying any charges.

Response: Could you please let your customers know the email subject that is used to communicate,

(a) the first, introductory mail that kick-starts the free trial?

(b) the subsequent email that announces the start of the charge (paid period)?

In my personal case, I have not received the first email. I received the 2nd email that announced the charge. The subject was, “Dear <name>, Welcome to Preferred Banking Program”

My contention is that it is fundamentally unethical to,

(a) send communication about a paid program with that email subject because,

(b) a bank usually sends as many as 5-10 emails per week, and

(c) if you expect all those emails, email fine prints to be read by all your customers, then

(d) one can only understand that as exploiting a loophole.

May I suggest the email subject, “Dear <name>, You will be charged from next quarter. Please read and action”? This means you have a clear intent to let your customers know that they are going to be charged. And that they have the choice and free will to do something about it.

b) Communicating the charges to customers at regular intervals. A welcome mail is sent to customers introducing them to the programme. Subsequently, the nominal fee is mentioned in the monthly bank statements, 12 of them, during the course of the free trial. Information on the charge is also available on our website, and with the Relationship Manager.

Response: This is fair. I haven’t seen this communication even once, but I fully realize that I should not hold my personal experience as a yardstick for anyone else. But, this does not explain why so many people seem completely surprised that there is a charge from the bank they do not recognize or understand? There are about 40 appended in screenshots above. I have personally seem over 1,000 since this blog post and tweets hit Officechai. If *all* those people miss seeing the communication, then there is something fundamentally wrong with the way this communication is handled.

c) Providing an exit option for those who do not wish to avail of these services.

Needless to say all this is in compliance with regulatory requirements.

Speaking of the Programme, well, I believe the benefits of the programme far outweigh the nominal fee of Rs 100 per quarter. While the benefits are detailed here: http://bit.ly/2nscKCP, the key ones are the following:

1) Discount of up to 100% on Locker charges

2) Unlimited usage of ATMs

3) Preferential pricing on loans

4) Waiver of charges for Non-Maintenance of the required Average Monthly Balance (AMB) on all accounts

While we believe this is a strong value proposition, a customer can exit anytime he chooses to by clicking a button.

Response: An ‘exit option’? Why not an opt-in? As in, ‘Joining option’? As in, why not pitch this ‘strong value proposition’ to your customers and let them consciously, voluntarily and with full awareness agree to the service, its terms and fees? Why ‘presume’ that your customers are dying to be part of a program and are incredibly eager to pay for it?

The ‘strong value proposition’ and the plethora of features is totally and wholeheartedly appreciated. Seriously. But, like the rest of the world, could you please ask your customers first, if they need it and if they are willing to pay for it? Instead of merely communicating that they will be charged for it eventually and use their silence as acceptance?

Also, many of your customers have been complaining on Twitter that they do not have this opt-out button (I was perhaps a lucky customer?). I’d love to see your response to them.

I know banks in their zeal do sometimes go overboard with emails, often the only channel left to communicate with customers. I also know it puts off some of us. But some of these mails, like the monthly statement, are a must-read. Wonder if there’s a way out?

Response: Email is not a problem. Please use email. Please use text messages. But please consider what email subject you are using. “Welcome to Preferred Banking Program” seems like it is designed to be ignored amidst 5-10 emails per week. On the other hand, “You will be charged from next week. Please take action” seems like what a customer-centric bank would use.

11.Relevant citings and excerpts from RBI, Banking Codes & Standards Board of India (BCSBI) and media

a. Excerpt from The Economic Times, September 12, 2006

b. Excerpt from The Economic Times, September 16, 2006

c. Excerpt from a speech by Dr Y V Reddy, Governor RBI 2006, in . (“Negative option marketing” is another term for ‘opt-out’)

d. Excerpt from a banking book titled, Banking Theory and Practice 21st Edition 2013 (by K C Shekhar and Lekshmy Shekhar)

e. Excerpt from Livemint article on banking reforms, by Tamal Bandyopadhyay

So, there is a change in the way HDFC Bank is communicating this opt-out offer.

One, the email subject is more direct and urgent. It now looks like,

![]()

Two, the email body has a more specific call-out to customers to opt-out with a hurried, breathless rejoinder on, ‘By the way, do you know what in the name of the good Lord you would be missing out if by any chance you saw this email AND read through it AND noticed this opt-out option? Here’s our favorite laundry list of world class benefits of the teeny tiny nominal program management fee we will start charging if, by a divine intervention, you did not see this email!‘

While it may seem like HDFC is listening and doing *something* about the problem I’m raising, this is a classic band-aid approach. This is a communication solution to a business and ethical problem. And the corporate communications head at HDFC admitted it in so many words… or, put those words into my mouth, which I respectfully threw back at him. Here’s that Facebook chatter between us.

So, summary: HDFC still presumes that customers are dying to pay the program management fees. The bank still presumes that if you do not do anything (that is, open the mail, read the mail or clicked on opt-out), that non-action will be used against you and the bank will start charging you.

Bottomline: The unethical part is about opt-out as a tactic, not the email subject. That was just one incidental point in the whole issue that HDFC has conveniently adopted as a major move. The dicey and unethical point about opt-out still exists.

AT LAST! A response (auto-response, nonetheless) from RBI. Let’s see where it leads to!

I had lodged a complaint with the Consumer Helpline about this unethical practice by HDFC. What I wrote:

HDFC Bank using negative option billing to charge customers without their knowledge. This means they send an email which states that they are being added to a paid program and if customers do not say they don’t want to be in the program, they will be charged every quarter.

This, plus all the supporting documents – countless other people who are complaining about the same, RBI and BCSBI’s rules against negative option marketing etc. I had not listed my account number anywhere in the complaint.

Yet, HDFC’s response is this. This, without knowing my account number. I assume they are trying to actively evade any question about lack of ethics and about the thousands of others who are asking the same question. I really hope some day they’d be forced to answer that actual question without being evasive. I have filed a counter complaint in return, once again, with the Consumer Helpline.